Typical mistakes in hedge fund valuation and risk assessment arise from neglecting their unique problems (see "The Unique Problems of Hedge Funds"). The distinct hedge fund valuation and risk management problems can be outlined as follows.

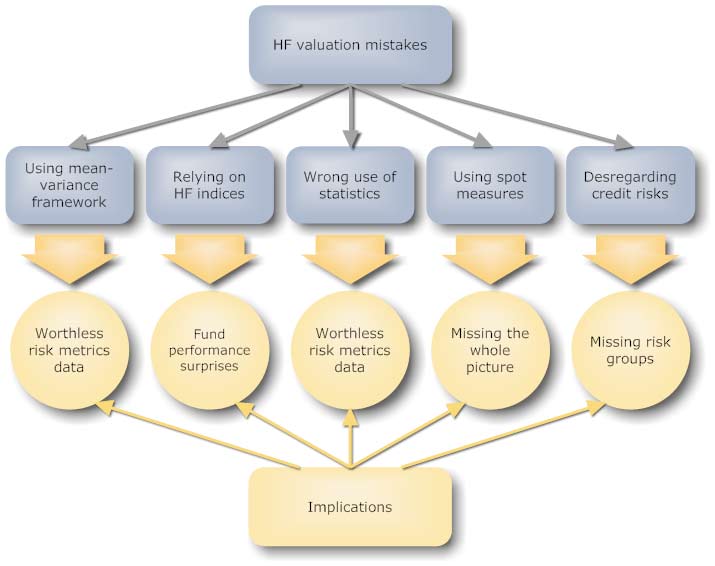

- Using the mean-variance framework for hedge fund risk assessment. This is by far the most common yet devastating mistake. Since hedge funds exhibit a high degree of non-normality of their distributions of returns, the risk measures based on the normality assumption (ex. the standard deviation and its derivatives like the Sharp or Sortino ratios) cannot be used.

- Using hedge fund indices as comparative benchmarks of individual fund performance. Hedge fund indices suffer from numerous biases (see Biases of Hedge Fund Data) and drawbacks. In brief, hedge funds may behave in discordance with their corresponding indices, while similar indices from different vendors may be even negatively correlated. For example, only 11.9% of Long/Short equity funds evidence correlation of over 0.5 with their corresponding index, while 8.3% exhibit a negative correlation.

- Using spot statistics, i.e. ignoring their dynamic behavior. Any spot measures are hardly informative, because only depict a single "risk shot" taken at a given time. Rolling charts should be used instead to get a correct picture of the trend over time.

- Ignoring the statistical significance of calculated metrics (correlation, r-squared etc). Though significance tests are a must for any academic research, this is rarely done in practice. The bottom line is that simple: any statistics meaningless, if show low significance levels.

- Taking into account too long historical return series. While long return series increase statistical validity of the computations, old historical observations are less relevant. Resolving that issue can be done by two ways. First, taking into consideration short series enough for statistical confidence tests. Second, applying more advanced techniques that use decreasing weights on past data (ex. the Hybrid VaR approach).

- Disregarding credit risks for multi-strategy funds. Analyzing historical performance data takes into account only market risks, though multi-strategy managers may be exposed to credit risks as well.

- Taking a low correlation between two assets as a definite sign of their neutrality. This is an entirely wrong concept. While a high correlation value most likely means traceable relationship (linear for the Pearson method), the opposite conclusion is incorrect. A low correlation may be caused by a non-linear connection between assets that cannot be identified by the applied methods.